海外で活躍するファンドマネージャーのニックが、定期的にマーケットのレポートを公開しています。ここでは私が日本語に翻訳して「ニックの見立てシリーズ」として連載していこうかと思います。

It has been a few weeks since we have published as your humble student of the markets has been on the road meeting investors. From our perch, there has been a notable shift in the prevailing bias over the period which our astute Italian friend has phrased “the big flip” – in essence the consensus trades that worked since late last year; peak inflation, rates, dollar weakness and EM out performance have “flipped” again since the start of February. The related consensus belief or fear of a hard landing in late 2022 has been undermined by resilient macro conditions, especially in the labour market, retail spending and some underlying components of inflation. The debate has pivoted from hard to soft or no landing at all.

この数週間、私は投資家に会いに行くため、この記事を発行することができませんでした。われわれの見立てでは、この間、市場の見方に顕著な変化があり、それをイタリアの識者が “ビッグフリップ (どんでん返し)”と表現しています。具体的には、昨年末から続いていたインフレ、金利、ドル安、新興国経済などのコンセンサスが、2月に入ってから再び「反転」したようです。

2022年後半にハードランディングが来るという恐れのコンセンサスは、特に労働市場、小売支出、インフレの基礎的要素などマクロ環境の回復力によって衰退しました。議論は、ハードランディングからソフトランディング、あるいは全くランディングしないという方向へと移っています。

Of course, an implication of the big flip, which has been reflected in short term interest rate markets is the re-pricing of July Fed fund futures by around 30 basis points since late January. Clearly there has also been a rise in terminal rate expectations and a higher-for-longer path for short term rates.

1月下旬以降、7月物のFF金利先物の価格が約30ベーシスポイント上昇したことは、このどんでん返しの影響が短期金融市場に現れたということです。金利上昇の予想到達点が上昇し、短期金利が長期的に上昇する道筋が形成されています。

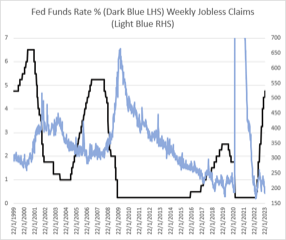

Put another way, the longer that significant portions of the US economy remain resilient, the higher interest rates need to rise to be restrictive. Despite 400+ basis points of tightening last year, policy is still not restrictive enough (typically rates must peak above the rate of inflation). Nevertheless, our sense is that the magnitude and speed of the current tightening cycle will eventually contribute to a hard landing in growth and profits. It is important to remember that policy lags by 12-18 months and will take time to impact the real economy and corporate earnings. For example, in previous cycles jobless claims (unemployment) after the peak in policy rates. Indeed, once the labour market starts to deteriorate more rapidly, the Fed is typically cutting the policy rate (chart 1).

別の言い方をすれば、米国経済の大部分が堅調を維持すればするほど、金利は上昇させる必要があります。昨年は400ベーシスポイント以上の引き締め政策を行いましたが、まだ十分に(インフレを)抑制していない(通常、金利のピークはインフレ率を超える必要がある)。とはいえ、現在の引き締めサイクルの規模とスピードは、最終的に成長率と利益のハードランディングのきっかけとなると我々は考えています。

ただし、政策の影響は12-18ヶ月遅れであらわれ、実体経済と企業収益に反映されるには時間がかかることを忘れてはなりません。例えば、過去の利上げサイクルでは、政策金利のピーク後に失業保険申請件数(失業率)が減少しています。実際、労働市場がより急速に悪化し始めると、FRBは政策金利を引き下げるのが一般的です(chart 1)。

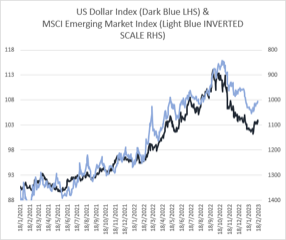

Another key aspect of the big flip has been the correlated reversal in dollar weakness over the past few weeks. The belief that inflation and short-term rates had peaked late last year, also contributed to a correction in the US dollar (which is itself a key component of broad financial and liquidity conditions). US dollar weakness also coincided with a recovery in emerging market assets (inverted on the time series below – chart 2). To be fair, the rally in EM was also driven by the rapid policy pivot and reopening from China. Although we would argue that both trends are reflexive with price and beliefs influencing risk perceptions in a feedback loop.

このどんでん返しのもう一つの重要な側面は、過去数週間のドル安の反転です。インフレと短期金利が昨年末にピークを迎えたとの見方も、ドル安の一因となりました(ドル安はそれ自体、幅広い金融・流動性の状況を表す重要な要素でもあります)。また、米ドル安は新興国資産の回復と重なりました(chart 2)。

公平に見て、新興国市場の上昇は中国の急速な政策転換と開放によってもたらされたものでもあります。しかし、われわれの主張は、この2つのトレンドが価格と市場のリスク認知に影響を与え、フィードバックループを形成する反射的なものだと考えています。

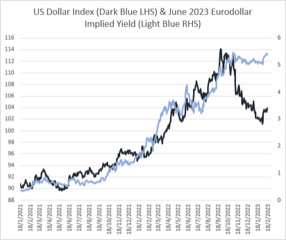

Tactically, the near-term risk for emerging markets (Asia) is that short term rate expectations in the United States, might warrant a larger rally in the US dollar back toward the October peak last year. While we are careful not to overstate the importance of naïve overlay relationships, higher short-term rates in the US, especially relative to other regions, might support a renewed phase of dollar strength (chart 3). It will probably lead to policy and financial conditions that are restrictive… eventually.

戦術的には、アジアの新興国市場の目先のリスクは、米国の短期金利予想が昨年10月のピークに近い米ドルの上昇を誘発する可能性です。我々はナイーブなオーバーレイ関係の重要性を誇張しないように注意していますが、米国の短期金利の上昇は、特に他の地域と比較して、ドル高の再来をサポートするかもしれません(chart 3)。それはおそらく、経済に制約的な政策・金融条件をもたらすだろう…いずれは。

To be fair, it is always important to ask: what is your quarrel with price? For now, the global risk proxy (the S&P500) has been resilient with macro conditions. However, our fear is that will lead to more policy tightening and rates that are eventually restrictive for risk assets. We trimmed net equity risk following the FOMC earlier this month in Asia Tech and growth equity. We suggest clients avoid speculative or profitless “growth equity”.

常に「市場価格に対する疑念は何か」と問うことが重要です。今のところ、グローバルなリスク代替(S&P500)は、マクロの状況に対して耐えています。しかし、私たちが恐れているのは、それがさらなる政策引き締めにつながり、最終的にリスク資産にとって制約となる高金利状況が発生することです。

今月初めのFOMCを受け、ポートフォリオのアジアIT企業と成長株で株式リスクを純減させました。投資家には、投機的、あるいは利益のない「グロース株」を避けることをお勧めします。